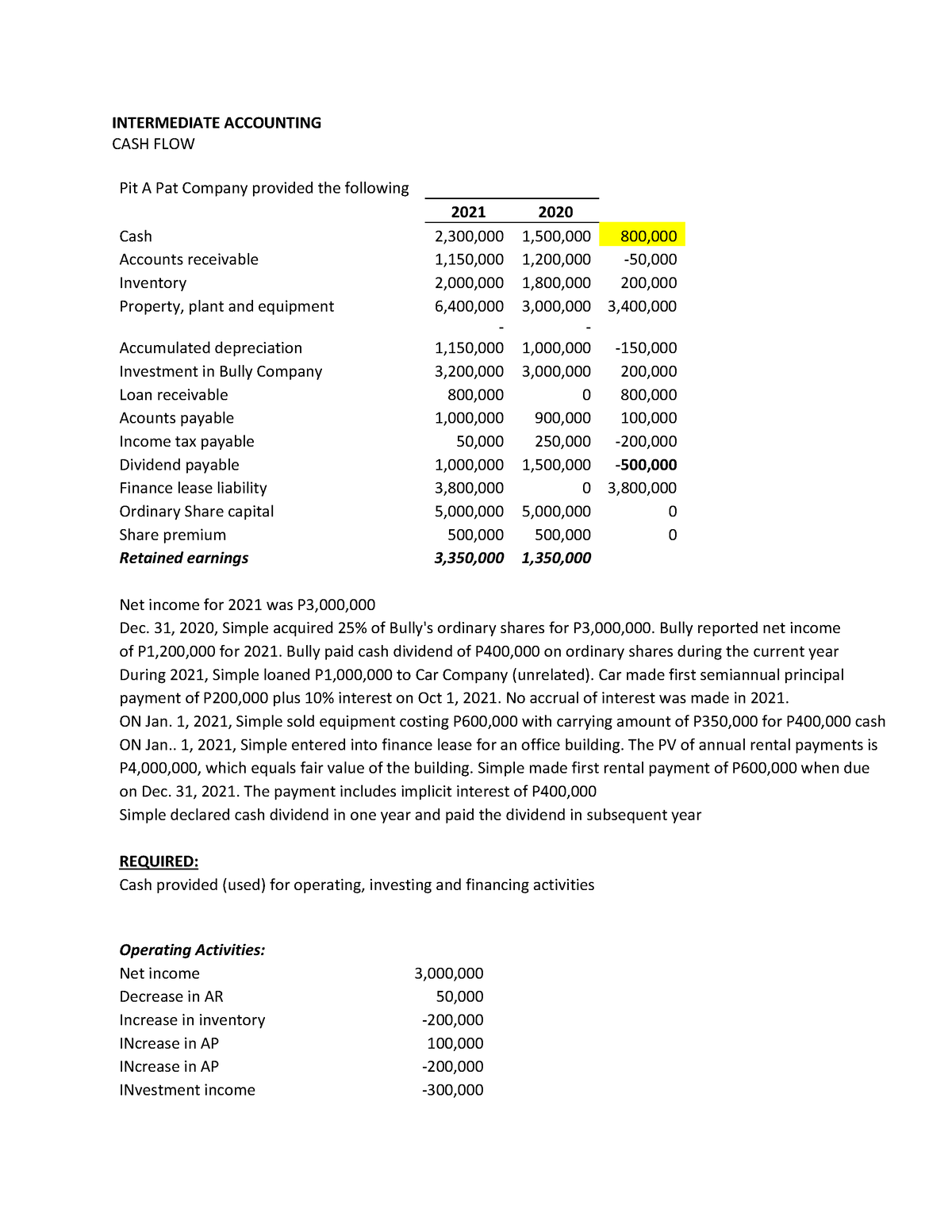

New meantime buy and you may improve money often have relatively higher desire costs and you will short payment terms and conditions

Domestic treatment loan mortgage

Getting house treatment affairs which do not also require purchasing or refinancing the property, consumers also can think a subject We Do-it-yourself Loan.

Dysfunction

Section 203k Domestic Rehabilitation Money (also known as domestic treatment money or mortgages) are fund created by private lenders which might be covered because of the Federal Construction Administration (FHA), an element of the U.S. Institution from Property and you will Metropolitan Invention (HUD).

- Pick otherwise refinance property

- Include the price of and also make solutions or improvements

- Become deductible closing costs

You could potentially get a rehabilitation loan since a 15- or 30-12 months fixed-rates home loan or given that a changeable-rates financial (ARM) off a beneficial HUD-recognized lender, while the mortgage deposit criteria is roughly step three% of the home purchase and you may repair costs. The degree of the loan start from a backup set aside regarding 10% in order to 20% of your own overall remodeling can cost you, familiar with defense any additional functions not within the brand new offer.

The total amount of your own financial depends on estimated property value your residence following renovation is accomplished, taking into consideration the expense of the job. A portion of the loan is used to pay for the latest purchase of the house, or even in the truth out of a beneficial refinance, to pay off people existing financial obligation. The remainder is positioned in the an interest-affect escrow membership on your behalf and you will put-out within the stages once the rehabilitation is done.

FHA necessitates that make use of at least $5,100 on qualified repairs or developments and you complete the fixes in this 6 months following the loan’s closing with regards to the extent off work to be completed. This first $5,100000 primarily discusses reducing building password violations, modernizing, or and work out health and safety-associated upgrades into house or its garage. You could include minor otherwise beauty products fixes following this specifications is actually came across, when the applicable. You cannot include developments to have commercial fool around with otherwise luxury affairs, eg tennis courts, gazebos, otherwise this new swimming pools.

If you are not going to live-in your house during construction, you can even loans doing half a year from home loan repayments during brand new repair period. On top of that, you can even act as the general company otherwise do the real repair really works your self, while you are accredited. Any money you save like that are used for cost overruns or additional developments. You’ll be refunded only for real thing can cost you, not on your own work.

House must be about a year-old, in addition to complete property value the house or property must slide in FHA home loan restrict towards city. The fresh new FHA limit mortgage maximum into the area is generally surpassed from the price of energy conserving improvements, additionally the mortgage is approved to own a growth as high as 20% from the restriction insurable home loan amount if the like an enthusiastic improve will become necessary to your installation of solar energy gadgets. Yet not, the complete home loan don’t meet or exceed 110 percent of one’s property value the property. The value of the home varies according to possibly (1) the worth of the property ahead of rehabilitation and price of rehabilitation, otherwise (2) 110 % of one’s appraised value of the home immediately after rehab, any kind of is quicker.

Point 203(k) treatment loans are supplied as a consequence of FHA-accepted mortgage brokers nationwide, including of several banks, coupons and you will mortgage relationships, credit unions, and home loan companies. In lieu of other FHA solitary-nearest and dearest mortgage loans, Part 203(k) borrowers dont spend an initial home loan advanced. Although not, loan providers can charge specific a lot more costs, such as for example a supplemental origination commission, costs to afford thinking from architectural https://paydayloancolorado.net/heeney/ data files and review of the new treatment bundle, and a top appraisal payment.

Treatment Finance: Preserving Money and time

Very home loan financial support arrangements give simply long lasting financing. Which is, the financial institution will not constantly intimate the loan and you can discharge the fresh new mortgage continues except if the condition and value of the house offer sufficient loan protection. Because of this, the purchase of a property that requires resolve is often an excellent catch-twenty-two state, as the financial will not give an extended-title mortgage to acquire our house before solutions try over, and solutions can not be over up until the home could have been purchased.

In such circumstances, homebuyers often have to adhere to an elaborate and you can costly processes, first obtaining capital to buy the home, following bringing a lot more capital with the rehabilitation really works, last but most certainly not least wanting a permanent mortgage once rehabilitation is carried out so you’re able to pay off the brand new meantime fund.

A part 203(k) treatment financing, but not, allows the latest debtor score one mortgage loan, in the a long-title fixed (or varying) rates, to invest in both the order and also the rehab of the house. Section 203(k) insured fund conserve borrowers time and money, and now have manage loan providers by permitting these to feel the mortgage covered prior to the matter and cost of the home can get provide sufficient safety.